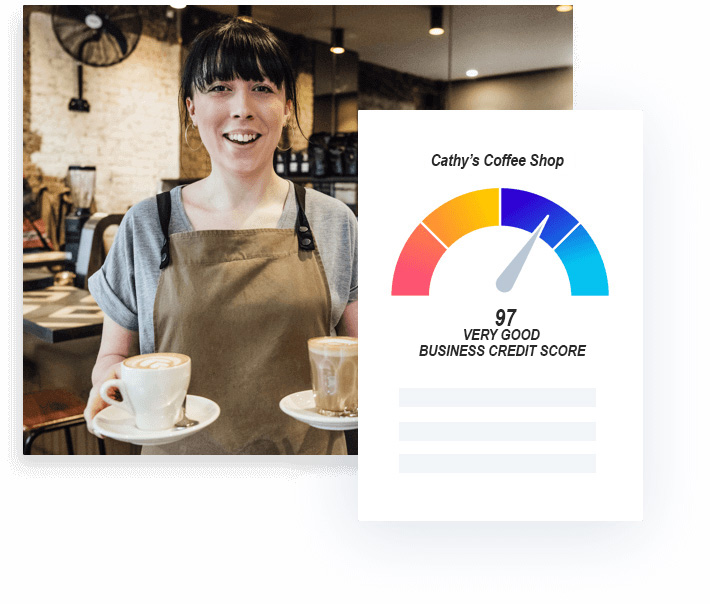

What Is a Business Credit Score?

Build your score, bring in the Benjamins.

A business credit score measures the financial stability of a business. The scores range from 0–100. Just as in personal credit, the major business credit reporting agencies (Experian, Equifax, and Dun and Bradstreet) use several common criteria to calculate business credit scores. However, unlike your personal credit score, your business credit score is available to the public. This includes lenders, vendors, and customers.

Business credit score criteria

Experian, Equifax, and Dun & Bradstreet all use these common indicators in their reporting of business credit scores:

- Years in business

- Credit lines applied for in the last 9 months

- Credit lines opened in the last 6 months

- Payment history for the previous 12 months

- Number of late payments

Benefits of strong business credit

A solid business credit score can help you:

- Qualify for small business loans, lines of credit, and credit cards

- Secure better rates and terms on financing

- Build a safety net that makes it easy to take out emergency loans or lines of credit if you fall on hard times

- Do business with new vendors and suppliers

Wait! Don't Forget Your FREE Guide!

How new businesses can get up to $150k in business credit that's linked to their SSN with no personal credit check!

It’s worth it to bring your score up

The primary reason that traditional lenders reject the majority of small business owners is a low business credit score. Building a strong credit score affords you more competitive interest rates and terms on funding, in addition to making it easier to take out emergency lines of credit, if needed. Keep in mind that vendors and suppliers also have access to your score and are more likely to do business with you if your credit is solid.

If your business is ever hit with hard times, a strong business credit score provides a safety net by making it easy to take out emergency loans or lines of credit. On top of that, vendors and suppliers are more likely to do business with you when your credit is solid.

The #1 reason that traditional lenders reject most small business owners is bad credit.

How to Build Business Credit

REGISTER YOUR BUSINESS AS A LEGAL ENTITY

Your business must be registered as a corporation or limited liability company (LLC) to be assigned a business credit score. This is a relatively easy process and can be done via LegalZoom. More importantly, establishing your business as a separate legal entity will also protect your personal assets from business liabilities.

OPEN A BUSINESS BANK ACCOUNT

A business bank account is imperative for keeping your business and personal finances separate, allowing you to continue to build business credit and providing an additional layer in protecting your personal financial assets from business liabilities. The business bank account should only be used for business expenses,however.

MAKE TIMELY PAYMENTS

Just as in personal credit, ensuring that your payments are on time is the best way to build and improve your business credit score. Lenders place extra emphasis on your payment history, so make sure it is stellar.

Suggestions for ensuring timely payments include:

- Utilizing auto-pay:Most recurring bills offer the option to have the amount deducted automatically from your bank account.

- Utilizing bill-pay reminders: Whether taking advantage of your own calendar or using reminders from software like Quicken or Microsoft Money, find a way to make sure that you are reminded when payment is due.

- Scheduling time each month to pay your bills: Make sure you have allotted a set time each month to pay your bills.

APPLY FOR A BUSINESS CREDIT CARD

Opening a business credit card enables you to build a history of on time payments in addition to improving your credit utilization ratio (how much credit is available to your business vs. how much you are actually utilizing). Most business credit cards also offer rewards.

APPLY FOR A CREDIT LINE/LOAN

Just as in credit cards, establishing a history of on time loan payments will also help to increase your business credit score. In turn, you’re more likely to qualify for better terms and lower rates in the future. There are a variety of options available depending upon your industry and situation.

REPAIR YOUR BUSINESS CREDIT SCORE

Unfortunately, a low business credit score almost always aligns with higher interest rates, which equate to higher finance charges on your balances. This takes away from the funds you need to grow your business. Below are 5 suggestions for improving your business score.

Check your business credit score on a regular basis

Many small business owners aren’t even aware that they have a business credit score. Fortunately, Your Lending Partner has outlined everything you need to know about accessing and checking your business score.

Check for mistakes

Just like personal credit reports, business credit reports can have errors, too. Pay close attention to payments that haven’t gone through or were never reported. Also make sure that you don’t have another business’s information reporting on your business credit report.

Make corrections

To correct mistakes, contact the credit bureau with evidence of the mistake and/or or contact the vendor and request that they update their reports with the bureau.

Take care of outstanding debts

Paying down outstanding debts will help raise your credit score. Make sure you are making payments on time. If you find yourself struggling to repay a loan or to pay off the balance of a credit card, discuss this with the lender before defaulting on the debt. Oftentimes they are willing to work with you.

Make payments on time

As we have stated many times before, making payments on time is the single most important thing you can do for your business credit.

YOUR INFORMATION IS SAFE

We do not sell or rent your personal contact information for any marketing purposes whatsoever.

SECURE CHECKOUT

All information is encrypted and transmitted without risk by using the Secure Sockets Layer protocol.

NEED HELP?

Toll-Free: (800) 400 2517

Local: (307) 222 0441

Fax: (307) 243 2447

Contact@YourLendingPartner.com

About Salient

The Castle

Unit 345

2500 Castle Dr

Manhattan, NY